Picture this: You’re scrolling through your news feed and see a breaking headline: “The Federal Reserve Cuts Interest Rates!”

If you are looking to buy a home or refinance, your heart probably skips a beat. You assume this means the 30-year fixed mortgage rate just dropped significantly, making your dream home much more affordable. You call your lender, excited for the good news, only to find out that current average mortgage rates barely budged—or worse, they actually went up slightly.

Tempted to throw your phone across the room? We get it. It’s incredibly frustrating and confusing.

As real estate professionals, we encounter this confusion almost daily. There is a massive misconception that the Federal Reserve has a big dial on its desk labeled “Mortgage Rates” that they turn up or down.

Today, with the help of this handy infographic, we’re going to bust that myth and explain what really moves the needle on your monthly payment in plain English.

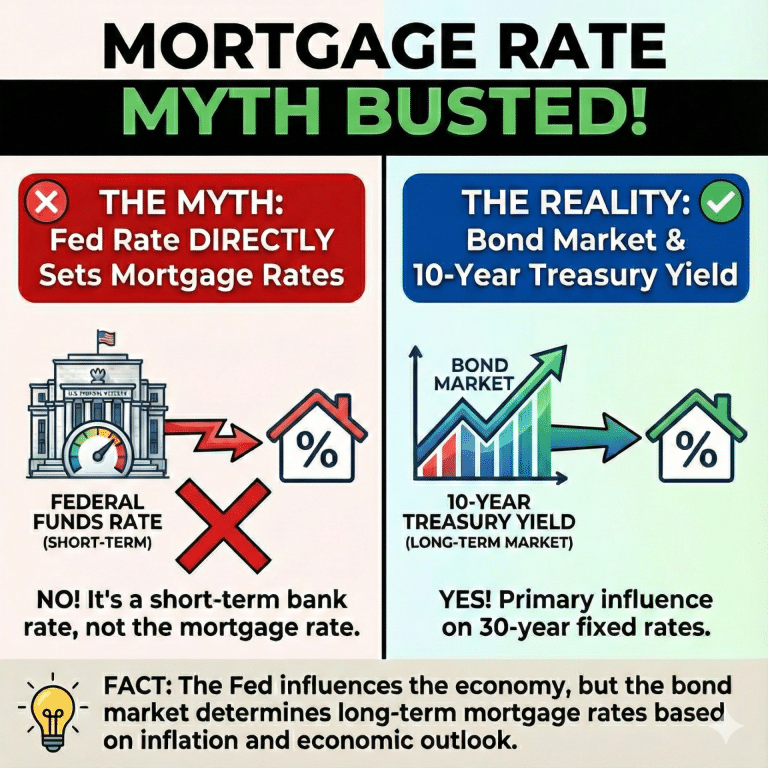

Let’s look at the graphic below. It perfectly illustrates the difference between what most people think happens versus what actually happens.

Look at the left side of the image. The common belief is that when the Federal Reserve (the building on the left) changes its rate, it sends a direct signal to the housing market, instantly changing the percentage rate on a home loan.

Why this is false:

The rate the Fed controls is called the Federal Funds Rate. This is a very short-term rate. It’s basically the interest rate banks charge each other to lend money overnight.

Think of it like this: If you needed to borrow $20 from a friend until tomorrow, the “interest” would be very low because the risk is low and the time is short. That’s the world the Fed operates in.

While a change in the Fed Funds Rate does affect things like credit card interest and car loans pretty quickly, it does not directly set the price of a 30-year mortgage.

Now, look at the right side of the image. This is how the financial world actually works.

A mortgage is a long-term commitment—usually 15 or 30 years. Because it’s a long-term loan, its interest rate is tied to long-term investment benchmarks.

The biggest benchmark for fixed-rate mortgages is the 10-Year Treasury Yield. This is the return investors get for buying U.S. government bonds that mature in ten years.

Why the 10-Year Treasury matters:

Investors who provide the money for mortgages want a safe, predictable return. They look at the 10-Year Treasury bond as the “risk-free” baseline. If they are going to lend money for a mortgage instead of buying a government bond, they demand a higher interest rate to make it worth the extra risk.

Therefore, mortgage rates almost always track the 10-Year Treasury yield up and down. You can see this clearly in historical data showing the correlation between the two. If the yield on the 10-year bond goes up, mortgage rates go up. If it goes down, mortgage rates go down.

The Connection: It’s All About Inflation

So, if the Fed doesn’t set mortgage rates, do they matter at all? Yes, absolutely. But their influence is indirect.

As the bottom “FACT” section of our infographic states: The Fed influences the economy, but the bond market determines long-term mortgage rates based on inflation and economic outlook.

Here is the simplest way to understand the relationship:

1. Inflation is the enemy of low rates. Lenders hate inflation because it eats away at the future value of the money they lend you. If investors fear inflation is rising, they will demand higher yields on Treasury bonds, which pushes mortgage rates up.

2. The Fed fights inflation. When the Fed raises its short-term rates, it’s trying to cool down the economy to stop inflation.

3. The Bond Market reacts. If the bond market believes the Fed is successfully fighting inflation, Treasury yields will often drop, bringing mortgage rates down with them—even if the Fed is currently hiking its own short-term rates!

Knowing that the bond market is the real driver of mortgage rates, here is our advice at MarketVision Real Estate:

1. Stop trying to “time the Fed.” Don’t make major life decisions based on a news headline about an upcoming Fed meeting. The bond market has usually already “priced in” whatever the Fed is about to do days or weeks in advance.

2. Focus on affordability, not just the rate. The rate is important, but so is home price, your down payment, and your monthly budget.

3. Talk to a pro. The bond market changes every single day. You can check the current 10-Year Treasury yield yourself, but interpreting what it means for your loan requires expertise.

If you are confused about the current rate environment and want to know what you can truly afford in today’s market, reach out to the team at MarketVision Real Estate. We can connect you with trusted local lenders who can cut through the noise and give you the real numbers.

Jacob Hartley, (2025, December12). Fed Rate vs Mortgage Rates: Busting the Real Estate Myth. https://www.marketvisionre.com/

A MarketVision representative will contact you within 24 hours to present you with their offer!